GGM Information Packs

Tax Codes to use from 6 April 2024

For 2024 to 2025 the basic Personal Allowance will be £12,570 for the whole of the UK. The threshold (starting point) for PAYE is £242 per week (£1,048 per month). The emergency code is 1257L for all employees.

This guidance tells you what you have to do to get ready and when to make the change to tax codes.

Tax Facts 2024/2025

- Personal Tax

- Pensions

- Investment Reliefs

- National Insurance Contributions (NIC)

- Employee Benefits

- Capital Gains Tax (CGT)

- Corporation Tax

- Capital Allowances

- Unincorporated Business Tax

- Property Taxes

- Value Added Tax (VAT)

- Inheritance Tax

- Trusts

- Key Deadlines

- Freeports

Tax Facts 2023/2024

- Personal Taxation

- Pensions

- Investment Reliefs

- National Insurance Contributions (NIC)

- Employee Benefits

- Capital Gains Tax (CGT)

- Corporation Tax

- Capital Allowances

- Unincorporated Business Tax

- Property Taxes

- Value Added Tax (VAT)

- Inheritance Tax

- Trusts

- Key Deadlines

- Freeports

Tax Facts 2022/2023

- Personal Taxation

- Pensions

- Investment Reliefs

- National Insurance Contributions (NIC)

- Employee Benefits

- Capital Gains Tax (CGT)

- Corporation Tax

- Capital Allowances

- Unincorporated Business Tax

- Property Taxes

- Value Added Tax (VAT)

- Inheritance Tax

- Trusts

- Key Deadlines

- Freeports

Tax Codes to use from April 2022

For 2022 to 2023 the basic Personal Allowance will be £12,570 for the whole of the UK. The threshold (starting point) for PAYE is £242 per week (£1,048 per month). The emergency code is 1257L for all employees.

This guidance tells you what you have to do to get ready and when to make the change to tax codes.

Worried about a Tax Investigation?

What is an HMRC investigation?

£35.5 billion is the estimated tax gap between what HMRC should collect and what it does collect. Small businesses and individuals account for over half of this amount.

To ensure tax compliance and to close this gap, HMRC undertakes tax and VAT investigations.

What prompts an investigation?

Working within a targeted sector, tip-offs from members of the public, or consistently late return submissions are just a few of the ways that an investigation is initiated by HMRC. However, random enquiries into tax affairs can and do happen. Whether you’re an individual taxpayer or business owner, an investigation is possible, and nobody is exempt.

A Guide to Making Tax Digital for VAT

Making Tax Digital (MTD) is the UK government’s flagship programme to make tax accounting easier for businesses and individuals.

As you might guess from the name, it does this by legislating the digitalisation of tax data and submission.

You might already use HMRC’s online services to complete tasks such as submitting your tax returns, for yourself and your business.

But MTD goes further than this. It requires the use of software for your accounting.

There are an incredible number of benefits for businesses and individuals when it comes to digitalising taxes. For example, cash flow is improved because you have a good idea throughout the year how much tax you owe. And using software for accounting means you spend much less time on admin, and more time doing what you love.

£1bn In Business Funding

The Chancellor has announced a raft of new measures to support UK businesses in response to the effects of the Omicron variant. Including:

• Statutory Sick Pay Recovery Scheme (SSPRS)

• New Hospitality & Leisure Sector Grants in England

• Continued support to the cultural sector.

• Other Businesses affected by COVID Disruption.

The Budget 2021 – Super-deduction

The new Capital Allowances offer

As a result of measures announced at this Budget, businesses will now benefit from four significant capital allowance measures:

• The super-deduction – which offers 130% first-year relief on qualifying main rate plant

and machinery investments until 31 March 2023 for companies

• The 50% first-year allowance (FYA) for special rate (including long life) assets until 31

March 2023 for companies

• Annual Investment Allowance (AIA) providing 100% relief for plant and machinery

investments up to its highest ever £1 million threshold, until 31 December 2021

• Within Freeport tax sites, companies can access new Enhanced Capital Allowances (ECA+)

and companies, individuals and partnerships can benefit from an increased level of

Structures & Buildings Allowance (SBA+) for investments until 30 September 2026.

The Business Recovery Manual - July 2021

In this booklet we have drawn together a series of updates on topics that business owners and taxpayers can use to support their efforts to re-establish their financial affairs after the dire effects of COVID disruption for the last fifteen months.

Much of what we suggest is that you consider your options carefully and plan accordingly. In this information pack we cover the following:

- Staying ahead of business challenges

- Why tax planning is a sound investment

- New business challenges in the post-COVID economy

- Business exit challenges in the post-COVID economy

- Creating multiple income streams

- Making the most of digital accounting

- Pension contributions - tax breaks

- Working from home – tax breaks

- Off-payroll working changes

- Not-so trivial benefits

- Extracting company profits

- New to self-employment?

- Utilising COVID tax losses

- Capital expenditure – the tax breaks

- Incorporating a property business

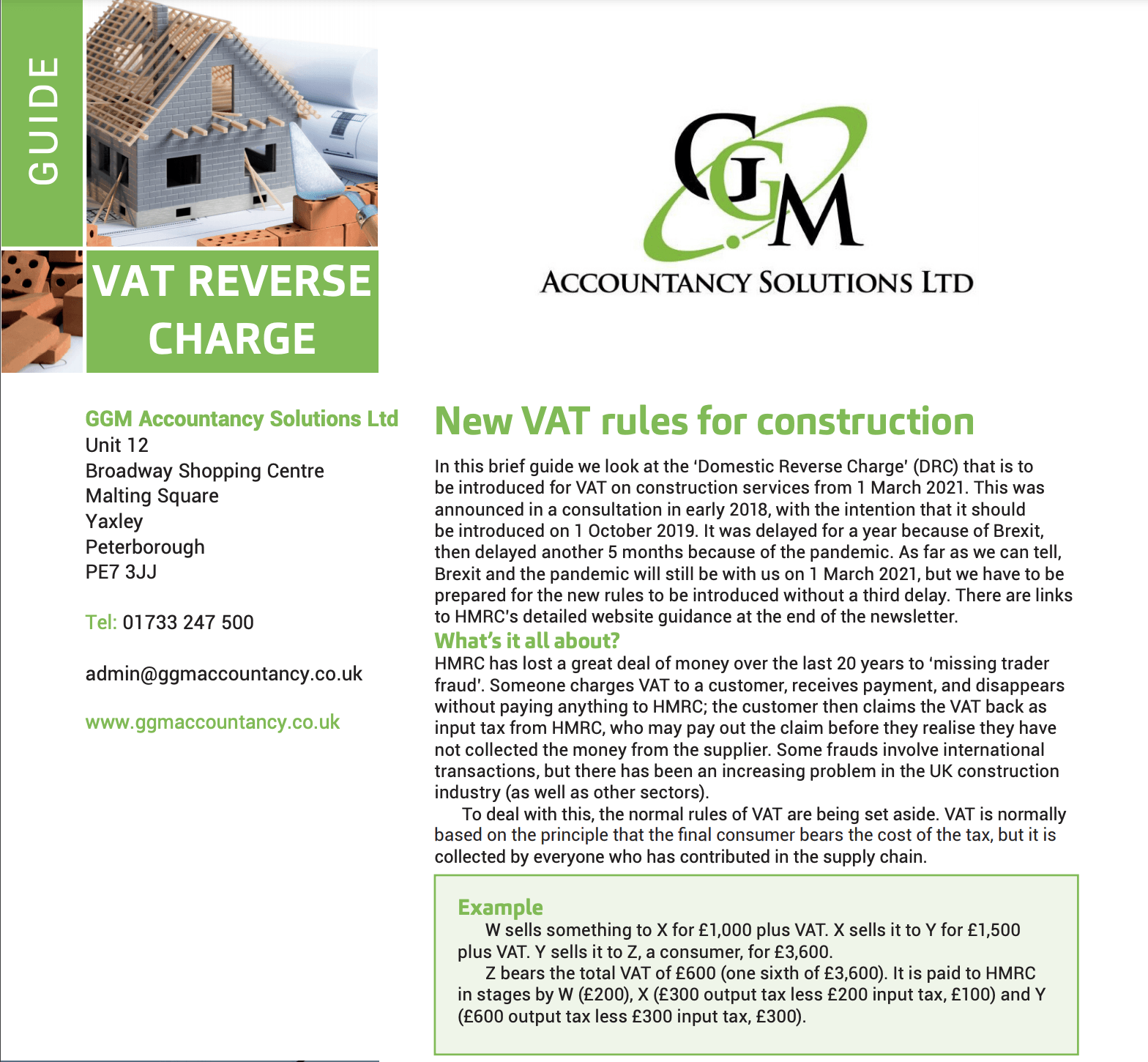

Reverse VAT Charge - February 2021

New VAT rules for construction In this brief guide we look at the ‘Domestic Reverse Charge’ (DRC) that is to be introduced for VAT on construction services from 1 March 2021. This was announced in a consultation in early 2018, with the intention that it should be introduced on 1 October 2019. It was delayed for a year because of Brexit, then delayed another 5 months because of the pandemic. As far as we can tell, Brexit and the pandemic will still be with us on 1 March 2021, but we have to be prepared for the new rules to be introduced without a third delay. There are links to HMRC’s detailed website guidance at the end of the newsletter.

What’s it all about? HMRC has lost a great deal of money over the last 20 years to ‘missing trader fraud’. Someone charges VAT to a customer, receives payment, and disappears without paying anything to HMRC; the customer then claims the VAT back as input tax from HMRC, who may pay out the claim before they realise they have not collected the money from the supplier. Some frauds involve international transactions, but there has been an increasing problem in the UK construction industry (as well as other sectors). To deal with this, the normal rules of VAT are being set aside. VAT is normally based on the principle that the final consumer bears the cost of the tax, but it is collected by everyone who has contributed in the supply chain.